It is a fact that women live longer than men. According to the World Health Organization, women live an average of six to eight years longer than men, but, despite this, women in the United States are more likely to have no retirement savings.

Women need to be prepared for the future, which means taking action with their finances today. This means to start saving, investing in diverse assets, and planning ahead for both the expected and unexpected.

Why is it important for women to start making financial plans?

One of the beautiful things about improvements to healthcare and living standards is that women in the US today are expected to live into their 90s, but, unfortunately, the cost of living is constantly on the rise.

Over an entire lifetime, women spend an average of over $300,000 on healthcare alone, while men typically only spend around $250,000. That money has to come from somewhere; for many people, living costs only get higher as you get into your senior years. Private rooms in retirement homes are surprisingly expensive, and you can expect all your other health and care costs to go up as well.

On top of that, the gender pay gap means that women can lose between $400,000 and $1.2 million over a 40-year career, which is one of the reasons women have fewer savings than men on average.

You don’t want to be working into your 80s, but that means having money set aside for some form of retirement. It’s not easy to achieve, but there are a few key things that you can do to make sure you are financially stable in the years ahead.

Work on saving money now

The most sensible and logical thing to start working on today is putting money aside so that you have a savings account prepared for when you eventually retire.

Of course, this is easier said than done, but it’s vital to future financial security.

Some essential tips that you can start working on today include:

- Pay off debts early

- Start with small savings, but be consistent

- Separate your savings from your spending money

- Utilize a savings account that has high interest

- Pay into your savings on payday

- Set achievable savings goals based on your income and outgoing expenses

To be realistic about how much you can save, you should review your budget. Figure out how much you spend on rent, bills, groceries, etc., over a month and compare that to how much is coming in.

Another critical part of establishing significant savings over time is preparing for the unexpected. Therefore, you should set aside a portion of your savings that can be used as an emergency fund in case you are temporarily without work or unforeseen circumstances require extra money.

You don’t want to lose everything you have been working towards because of a health issue, a gap in your work, or something as mundane as an engine malfunction in your car.

Balance your portfolio

Having one single pot full of your savings is helpful, but it is far from financially secure. Instead, it would help if you looked to diversify your assets so that your wealth is well-balanced between cash, stocks, and bonds.

Factors outside of your control, like inflation, can significantly reduce the value of the money you’ve saved up – so you want to invest in other liquid assets that can retain their value over time.

Valuable liquid assets can include:

- Treasury bills and treasury bonds. These are highly stable and highly liquid investments backed by the US government

- Bonds. You can hold your bonds until their maturity date, or you can trade them on the secondary market if you need the money quickly

- Stocks. You can sell equities on stock exchanges and purchase publicly traded stocks

- Exchange traded funds (ETFs). These investment funds trade like stocks and are less risky than individual stocks and bonds

- Mutual funds. These are easy to diversify but can only be sold at one time of day, so they are slightly less liquid

Remember, any investment you need to purchase (such as stocks or bonds) is a risk, and its value will change over time. As a result, you can sell for less than you originally paid.

Ideally, you want assets that will be relatively quick to sell and convert into usable cash. But some assets can make it harder to get your money out, even though they are still pretty safe.

Liquid assets include:

- Real estate. While a healthy investment in many markets, it can take a long time to get your money back through a sale

- Stock options. These are very valuable, but you must stay with a company for a long time before you own the stock itself

- Private equity. These investments, like venture capital, can offer large returns but are generally quite restrictive in terms of when you can sell your shares

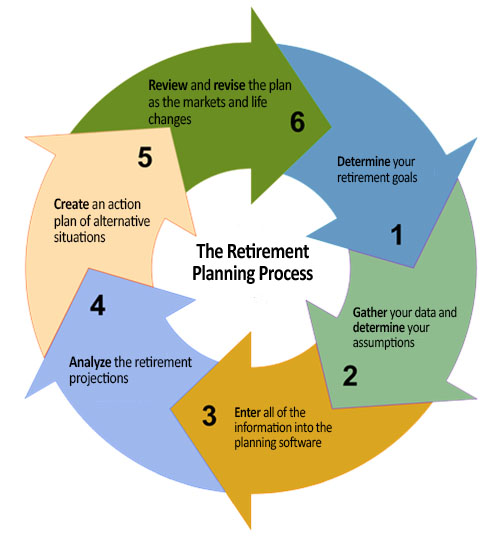

If you don’t know much about the world of portfolios, it would be worth speaking to a financial advisor who can help you understand where your money could be best used and develop a robust retirement plan.

Invest in insurance

The future is full of unknowns, and insurance is a critical way to prevent yourself from falling into debt.

While working, take advantage of all the benefits your workplace provides – like life insurance, health insurance, and disability insurance. However, paying close attention to how your coverage works is essential, as many plans expire once your employment ends.

Consider investing in independent insurance policies that you can trust in the long term and planning for age-related circumstances with things like long-term care insurance. For example, Medicare is beneficial in many ways but doesn’t cover services like in-home care or nursing homes.

Wait to cash in

You shouldn’t have to work any longer than you need to, but the longer you work, the less time you have to rely on your retirement savings.

You can also choose to delay your Social Security benefits, which will increase the amount of money you receive when you do choose to start taking advantage of them.

If you wait to get Social Security until you are 70, you will get the most money from it.

Summary

So, how should women financially plan for retirement and potentially live longer than most men?

You must start putting money into savings as soon as possible and consistently increase those savings over time. You should also make sure to balance out your financial profile so that you have a variety of assets to draw from when the time comes.

It’s also important to be ready for the unexpected, so you should buy insurance and save money for emergencies.

It is almost always worth sitting down with a financial adviser. That way, you can be sure that you have a robust plan that will allow you to enjoy a long, comfortable retirement.

Leave a Reply